Multivariate Linear Regression¶

Learning Objectives¶

- Multivariate linear regression

- Vector implementation

- Input Scaling

- Concepts of machine learning: learning, cost function, gradient descent

- Basis functions

Problem formulation¶

Supervised learning: regression¶

- $m$ observations (training examples) with

- $n$ Features:

- $i$-th training example

- ${\bf x}^{(i)}= \{ x_1^{(i)}, x_2^{(i)}, \dots, x_n^{(i)}\}$

- $x_j^{(i)}$: value of the feature $j$ for the $i$-th example

- $1 \leq j \leq n$ (univariate case $n=1$):

- $i$-th target value $y^{(i)}$

- $i$-th training example

Goal: prediction of $y$ for a new $\bf x$.

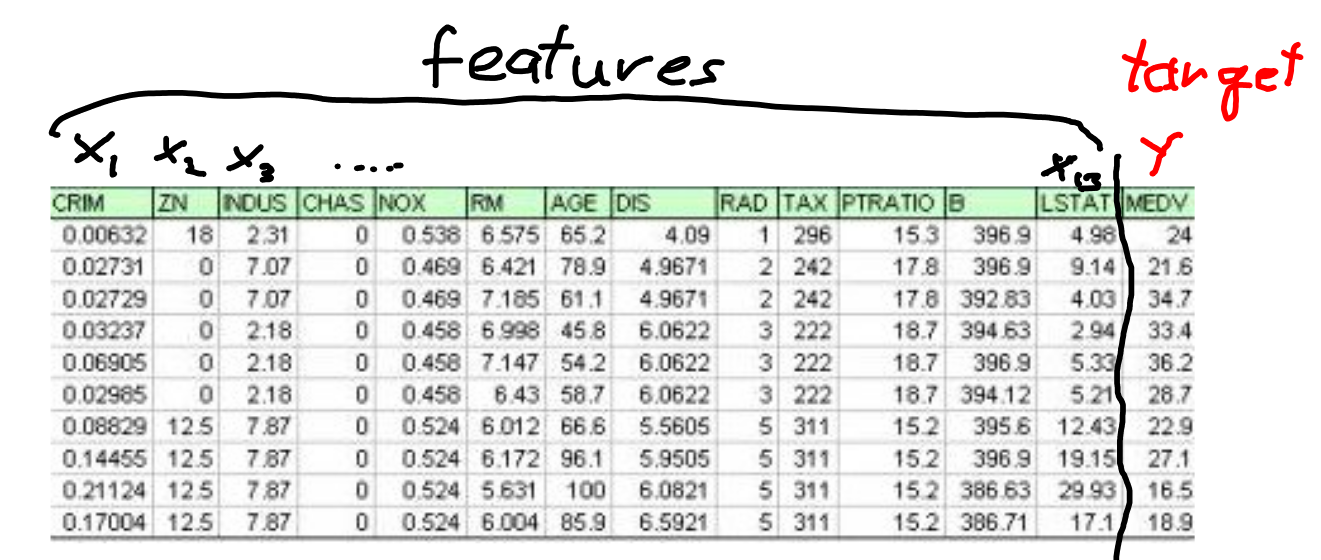

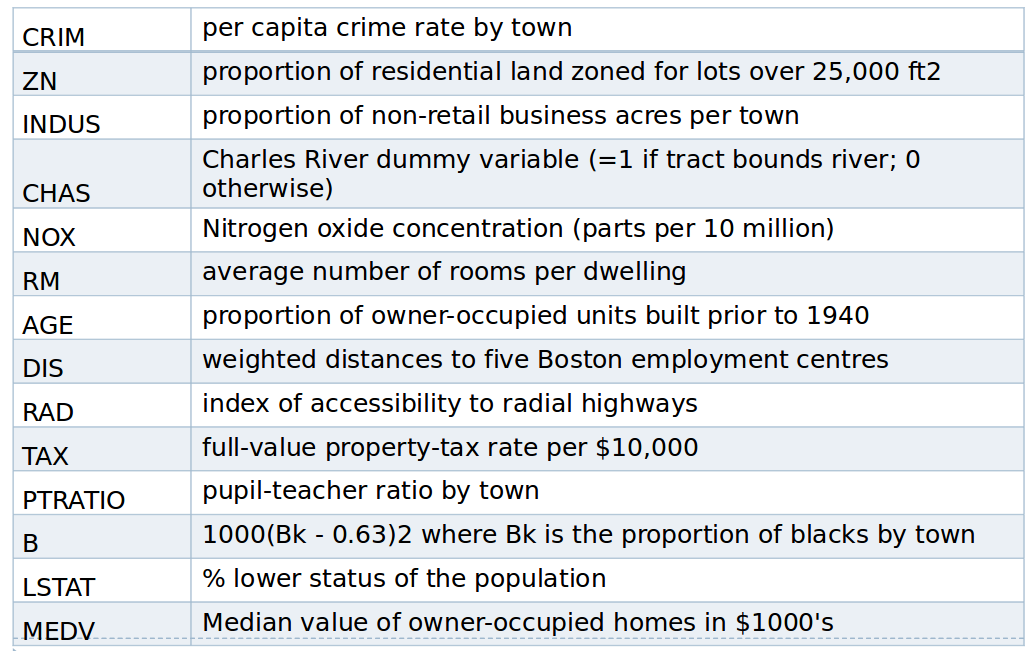

Example Boston data¶

Boston feature names¶

#load data

from sklearn.datasets import load_boston

boston = load_boston()

# feature names

#boston.feature_names

# features (vec x)

#print(boston.data)

# house price (y)

#print(boston.target)

Linear model¶

- linear with respect to the parameters $\theta_j$

- (for now) linear with repect to $x_j$

print (boston.DESCR)

# feature names

print(boston.feature_names)

# features (vec x)

print(boston.data)

# house price (y)

print(boston.target)

Vector formulation¶

Hypothesis: $h_{\theta}(\vec{x}) = \vec{\theta}^T \cdot \vec{x} = \theta_0 x_0 + \theta_1 x_1 + \dots \theta_n x_n $

- with $x_0 = 1$

- $n+1$ parameter: ${\vec{\theta}}^T = ( \theta_0, \theta_1, \dots , \theta_n ) $

for convenience we use $\theta$ as symbol for all $\{ \theta_0, \theta_1, \dots \}$

Cost function and gradient descent¶

Minimization of the cost function $J$¶

$$ J({\theta}) = \frac{1}{2 m} \sum_{i=1}^m (h_{\theta}(\vec{x}^{(i)}) - y^{(i)})^2 $$Recap: Gradient Descent¶

Repeat until convergence:

$$ \theta_j \leftarrow \theta_j - \alpha \frac{\partial}{\partial \theta_j} J(\theta) $$Vector form of the update rule¶

with the definition of the gradient $$ grad(J(\theta)) = \vec \nabla J(\theta) = \left( \begin{array}{c} \frac{\partial J(\theta)}{\partial \theta_0} \\ \frac{\partial J(\theta)}{\partial \theta_1} \\ \dots \\ \frac{\partial J(\theta)}{\partial \theta_n} \end{array}\right) $$

$$ \vec \theta^{neu} \leftarrow \vec \theta^{alt} - \alpha \cdot grad(J(\theta^{alt})) $$

Partial derivates for linear regression¶

\begin{align*} \frac{\partial}{\partial \theta_j} J(\theta) &= \frac{\partial}{\partial \theta_j} \frac{1}{2m} \sum_{i=1}^m (h_\theta(\vec x^{(i)}) - y^{(i)})^2 \\ & = \frac{\partial}{\partial \theta_j} \frac{1}{2m} \sum_{i=1}^m (\vec \theta^T \cdot \vec x^{(i)} - y^{(i)}) ^2 \end{align*}So we have update rules for all $\theta_j$ ($0 \leq j \leq n$):

$$ \theta_j \leftarrow \theta_j - \alpha \frac{1}{m} \sum_{i=1}^m (\vec \theta^T \cdot \vec x^{(i)} - y^{(i)}) x_j^{(i)\ } $$Vector form of the update rule for linear regression¶

$$ \vec \theta^{new} \leftarrow \vec \theta^{old} - \alpha \frac{1}{m} \sum_{i=1}^m (\vec \theta^T \cdot \vec x^{(i)} - \ y^{(i)}) \vec{x}^{(i)} $$Feature Scaling¶

If the features have different order of magnitude: the learning will be very slow (see e.g. here on pages 26-30).

A remedy is rescaling of the features.

Idea: values of all {\it Features $x_j$) should be in the range: $$ -1 \lesssim x_j \lesssim 1 $$

Z-transformation¶

$$ x_j' = \frac{x_j-\mu_j}{std(x_j)} $$with

- mean of $x_j$: $\mu_j = \overline{x_j}= \sum_i x_j^{(i)} / m $

- standard deviation of $x_j$: $std(x_j) = \sqrt{var(x_j)}$

- variance of $x_j$: $var(x_j) = \overline{(x_j - \mu_j)^2} = \overline{x_j^2} - \mu_j^2$

For all features $x_j'$ the mean is 0 and the standard deviation is 1.

Implementation and practice¶

Data matrix (design matrix)¶

Train data as matrix ${\bf X}$ with $X_{ij} \equiv x_j^{(i)}$

- each rows $i$ corresponds to a training example $\vec x^{(i)}$

- each column $j$ corresponds to the $j$-th feature

- with $x_0^{(i)} = 1$

Prediction can be done for all data by:

$$\vec{h}({\bf X}) = {\bf X} \cdot \vec{\theta}$$import numpy as np

# dummy values

X = np.random.randn(700,4)

theta = np.array([2.,3.,4.,5.])

# e.g.: with 3 features and 700 training data with numpy:

print (X.shape)

print (theta.shape)

h = X.dot(theta)

print (h.shape)

Vectorisierte Form of the update rule with Data Matrix $\bf X$¶

From the vectorised form of the update rule

$$ \vec \Theta^{new} \leftarrow \vec \Theta^{old} - \alpha \frac{1}{m} \sum_{i=1}^m (h(\vec x^{(i)}) - y^{(i)}) \vec{x}^\ {(i)} $$we get with the data matrix ${\bf X}$ $$ \vec \Theta^{new} \leftarrow \vec \Theta^{old} - \alpha \frac{1}{m} {\bf X^T} \cdot ( \vec{h}({\bf X}) - \vec y) $$

in numpy:

theta = theta - alpha * (1.0 / m) * X.T.dot(h - y)For testing if the gradient descent implementation works¶

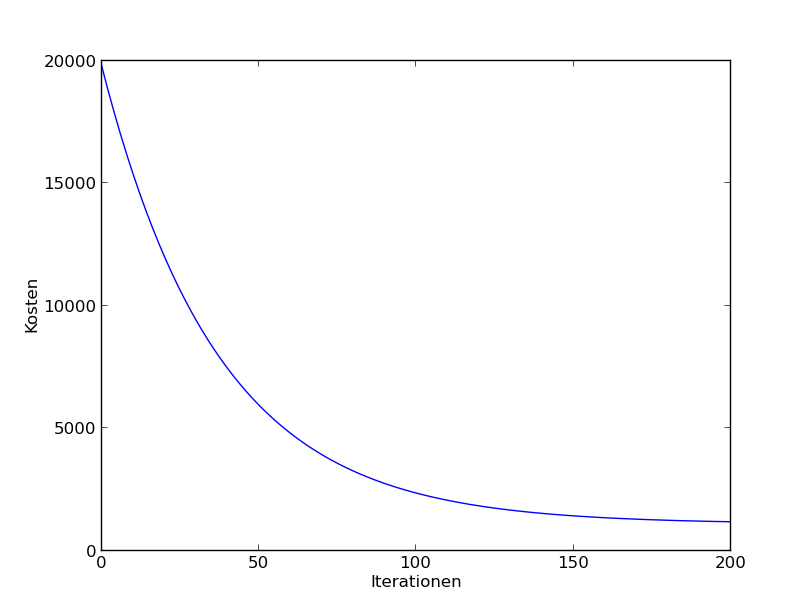

Remember the goal is to find the $\text{min}_\theta J(\theta)$

Plot $J(\theta)$ over the iterations: $J(\theta)$ must become smaller in each iteration (for full batch learning).

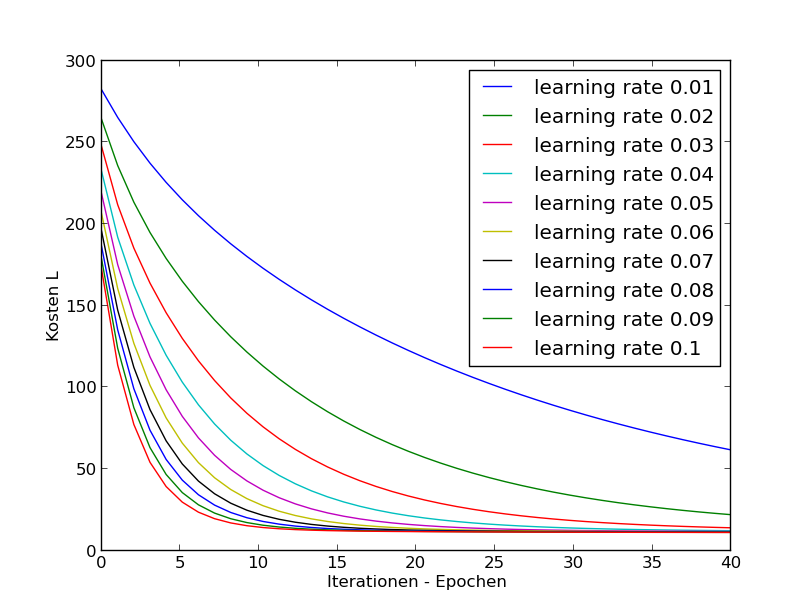

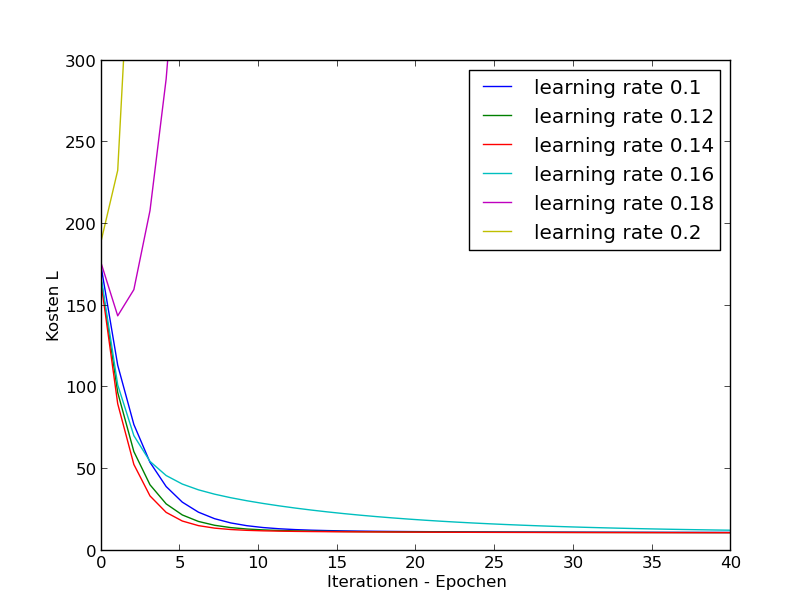

Learning Rate $\alpha$¶

How to choose $\alpha$?

Look at the progress during learning for different values of $\alpha$!

to small values for $\alpha$:

to large values for $\alpha$:

If $\alpha$ is to small $\Rightarrow$ smale convergence.

If $\alpha$ is to large $\Rightarrow$ $J$ grows or (oscillation or suboptimal progress). Wenn α zu groÿ ist, eventuell keine Konvergenz:

Try different $\alpha$'s (on log-space) or e.g.: 0.003, 0.006, 0.009, 0.03, 0.06, 0.09, $\dots$

Note: With feature scaling learning yield modified parameters : $\theta_0'$ und $\theta_1'$

\begin{align*} h(x) & = {\theta_0}' +{\theta_1}' x' \\ & = {\theta_0}' +{\theta_1}' \cdot \frac{x - \mu}{\sigma_x} \\ & = ({\theta_0}' - {\theta_1}' \cdot \frac{\mu}{\sigma_x} )+ \frac{{\theta_1}'}{\sigma_x} \cdot x \end{align*}i.e. \begin{align} \theta_0 & = \Theta_0' - \theta_1' \cdot \frac{\mu}{\sigma_x} \ \theta_1 & = \frac{\theta_1'}{\sigma_x} \end{align}

Basis functions¶

So far: The model is linear in respect to the input:

$$ h_\theta ({\vec x}) = \theta_0 + \sum_{j=1}^n \theta_j x_j $$Extension: Replace the $x_j$ with basis functions $\phi_k ( {\vec x}) $:

$$ h_\theta (\vec x) = \theta_0 + \sum_{k=1}^{n'} \theta_k \phi_k ( {\vec x}) $$Still a linear model. It's linear with respect to the parameters $\theta_j$

Examples for basis functions¶

Polynoms: $$ \phi_k ( {\vec x}) = x_1^2 $$

$$ \phi_{k'} ( {\vec x}) = x_1 \cdot x_3 $$``Gaussian Basis Functions''

$$ \phi_{k''} ( {\vec x}) = \exp\{ - \frac{(x-\mu_j)^2}{2 \sigma_j^2}\} $$(New) Features¶

- Transformation of the raw data $\vec{x_i}$ to features $\vec \phi(\vec x_i)$

Example: prediction of the price of land:

raw data: length $x_1$ and width $x_2$. \

instead: $h_\theta = \theta_0 + \theta_1 \cdot length + \theta_2 \cdot width $ \ \vspace{1cm}

use the ``area'' as feature $\phi_1$: $area = length \cdot width$

$$h'_\theta = \theta_0' + \theta_1' \cdot area $$

Polynominal regression¶

Exercise: Vector implementation of gradient descent¶

Note:

- The implementation should work with an arbitrary number of features.

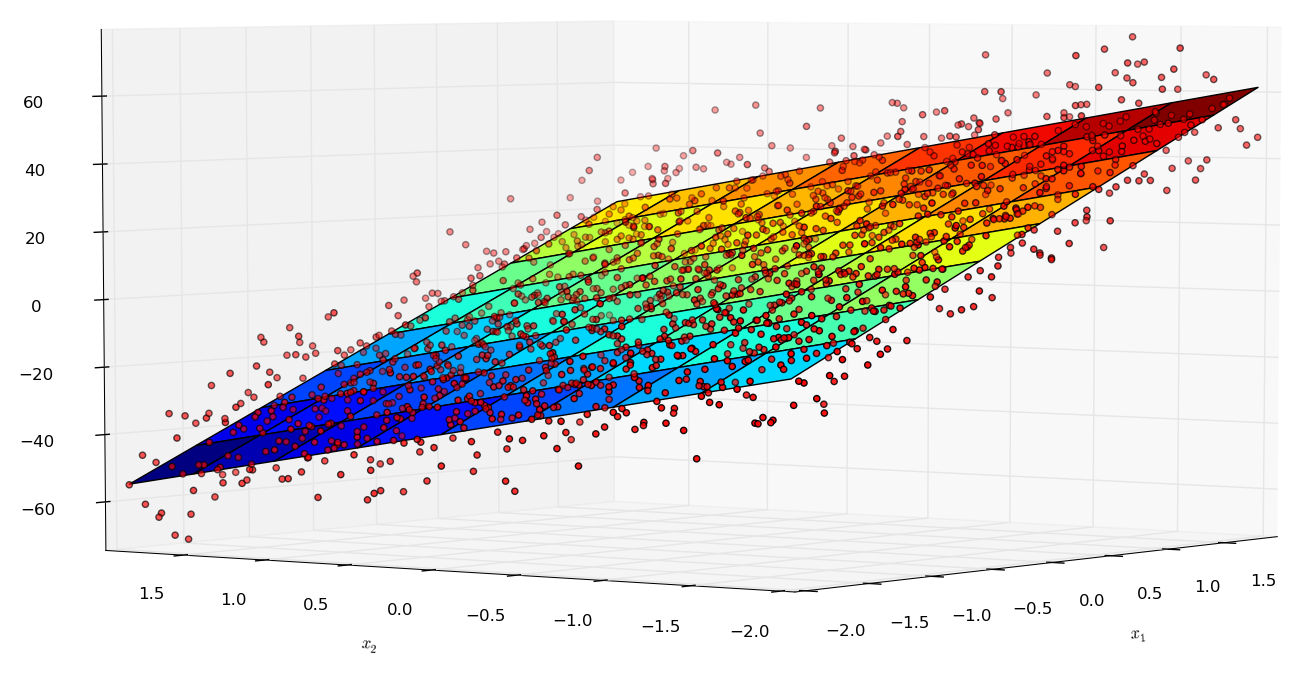

- Generate artificial data for the design matrix $\bf X$ with two features $x_1, x_2$ (or three with fixed $x_0=1$)

- Implement a

get_linear_hypothesisfunction:>theta = np.array([1.1, 2.0, -.9]) > h = get_linear_hypothesis(theta) > print (h(X)) array([ -0.99896965, 20.71147926, ... - Target values:

- Use the

get_linear_hypothesisfunction for generating y-values (add gaussian noise) - Plot the x1-x2-y data points in a 3D-plot, see http://matplotlib.org/mpl_toolkits/mplot3d/tutorial.html

- Use the

Implement the 'get_cost_function(x, y)' python function:

> j = get_cost_function(X, y) > print (j(theta)) > 401.20 # depends on X and yImplement gradient descent.

Implement a function for the update rule:

> theta = compute_new_theta(x, y, theta, alpha)Implement a function

gradient_descent(alpha, theta, X, y).thetaare the start values for $\vec \theta$. The function applies iterativelycompute_new_theta. Use an arbitrary stoping criterion.

Plot the progress (cost value over iterations) für 5B

Plot the optimal hypothesis in a graph with the data (see 3B).

Literature:¶

- Andrew Ng: Machine Learning. Openclassroom Stanford University, 2013

- C. Bishop: Pattern recognition and Machine Learning, Springer Verlag 2006